Oil prices and price gouging: Deconstructing the price of gas

REAL ECONOMY BLOG | June 09, 2022

Authored by RSM US LLP

Rising energy prices have stimulated a fierce debate around inflation and what is behind the surge in gas prices. Are companies taking advantage of a stressful time in the economy and raising prices more than they need to?

Accusations of price gouging and corporate greed now permeate the public discussion and are entering the debate about public policy. So what’s going on?

To begin with, it helps to understand what happens to a barrel of oil as it goes from the well to the consumer. There are many costs added along the way, from refining to retailing to federal, state and local taxes.

Such an analysis shows that the answer is more nuanced than notions of price gouging or corporate greed. Rather, the analysis shows that the primary cause of the prices increases can be traced to the significant impact of Russia’s invasion of Ukraine on global energy markets and OPEC’s continuing influence over those markets.

In the end, the impact of these broad, global market forces far outweighs whatever influence retailers or refiners have on the prices that consumers pay at the pump.

From production to consumption

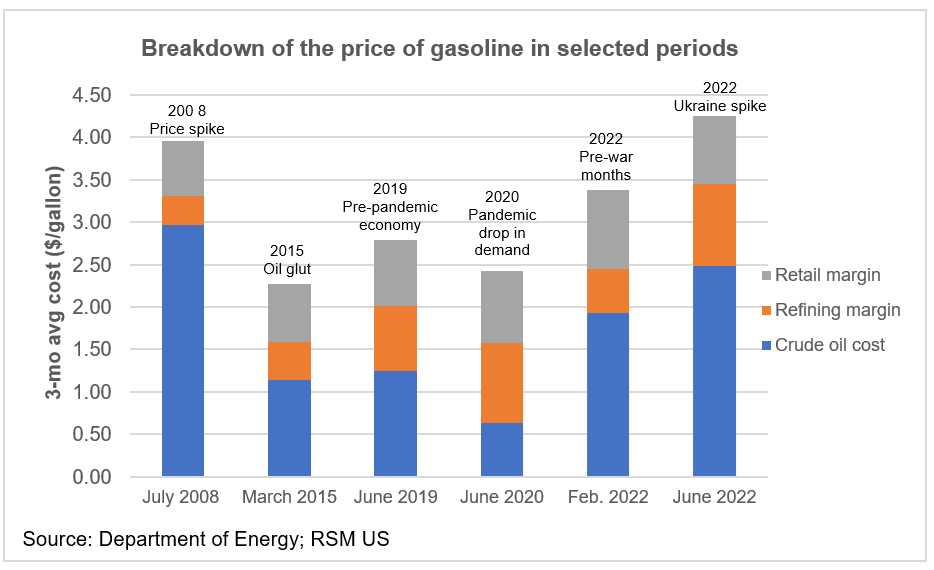

Consider the three-month average price of a barrel of West Texas Intermediate crude. Through the end of May, it was $106.52.

Given that there are 42 gallons in a barrel of oil, that implies a price of $2.53 a gallon. But the average price per gallon of regular unleaded gasoline was $4.26 at the time. The $1.73 spread reflects refiner margins, retailer margins, federal taxes and varying state and local taxes.

Those prices continued to increase into June as WTI surged to $120.64 a barrel, or an implied price of $2.87 a gallon. When the national average price of gas reached $4.95 per gallon by June 8, the spread increased to $2.08 a gallon—an outsized increase.

A big contributor to the surging price of gas is the near-doubling in the cost for refining crude into gasoline. There were shortages at Gulf Coast refineries during the regular spring maintenance period as well as outages in Europe. And the implementation of European Union sanctions against Russian oil helped push up the cost of crude as well.

All of this has an effect on the cost of goods and services downstream in the economy.

A global market for fossil fuels

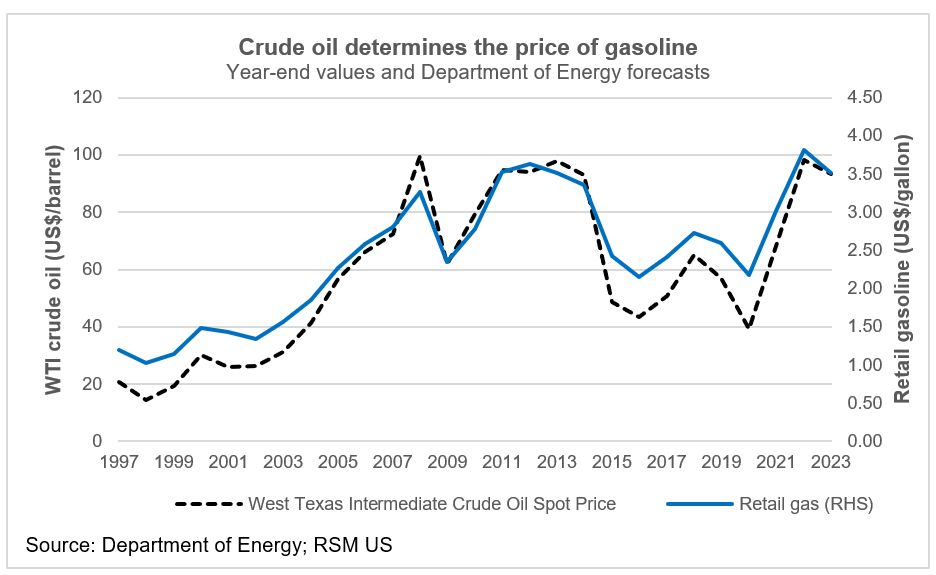

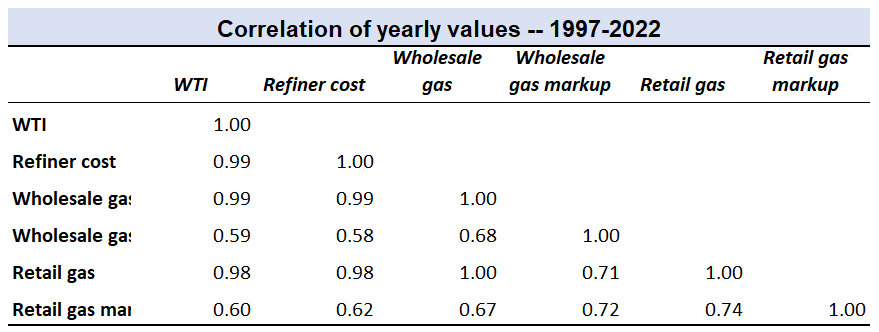

The price you pay for a gallon of gasoline at the pump is determined by the global market for crude oil. Using annual data—compiled by the Department of Energy from 1997 through 2022—we show a near-perfect correlation between the price of crude oil and both the wholesale and retail prices of gasoline.

That means that if the supply of crude oil is less than the demand for fossil fuels, then the price of gasoline will rise. If there is a glut of crude, then the price of gasoline will fall accordingly.

And because crude oil is fungible for all practical purposes, the price of crude is arbitraged within a global market. That means that prices for West Texas Intermediate crude oil paid by refiners in Louisiana will depend on the supply of and demand for crude produced in the Middle East, Russia, Venezuela as well as the Permian Basin.

Price markups

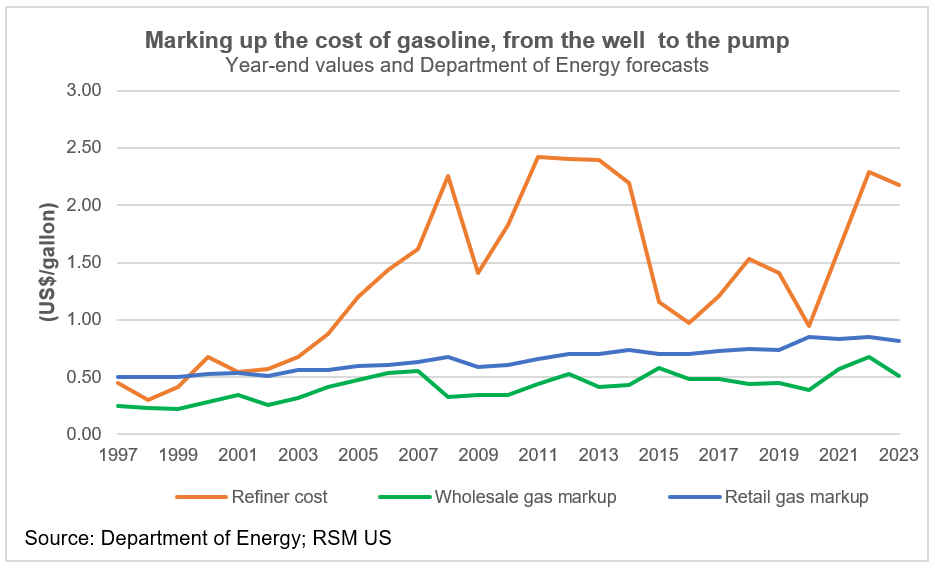

The intermediate markups imposed by refiners (which create the wholesale price of gas) and retailers have been increasing over time. That would be expected given the general trend of rising prices in a vibrant economy.

So while the price of crude on the global market has been volatile, the markups by wholesalers and retailers have been subdued by comparison. Wholesale markups increased from 25 cents per gallon to 50 cents a gallon, and retail markups increased from 50 cents to 85 cents over the same 25 years—hardly the stuff of price gouging.

The cost of drilling a new well

With oil prices so high, why haven’t U.S. producers responded with significant investments in drilling new wells?

Estimates of the breakeven cost of drilling a new well in the Permian Basin are around $50 a barrel. The implication is that at current prices, producers could conceivably flood the U.S. market with barrels of crude to be refined at U.S. facilities and sold to American consumers. But that argument ignores two important factors.

The price of WTI has dropped to $40 a barrel twice in the past six years, making investors wary.

First is the financial willingness to invest in a century-old industry. The price of WTI has dropped to $40 a barrel twice in the past six years, making investors understandably wary. Who would put money down on the chance those price drops won’t occur again?

The second factor is the market-based setting for the supply-side of the pricing equation. Let’s start with the lack of excess capacity among the world’s producers, most of whom are state actors. With the exceptions of Saudi Arabia and the United Arab Emirates, most producers are already at capacity. And Russian oil is being taken out of the picture, at least for the developed economies in the West.

The Saudis and the Russians are special cases. Keep in mind that the breakeven cost for existing wells in Saudi Arabia is estimated in the range of $25 per barrel or less. But keeping prices for crude above $50 per barrel would attract competition from non-OPEC producers.

In recent decades, it was in OPEC’s best interest to keep fossil fuel prices low enough to hold onto market share and to keep U.S. consumers driving inefficient vehicles.

A two-pronged approach

If anything, the recent surge in gas prices reinforces the need for a two-pronged approach to domestic energy policy.

- Don’t ignore fossil fuels: First, investment in the production of fossil fuels like natural gas, as well as oil, to bridge the long transition to renewable sources of energy will need to increase in the near term. Domestic refining capacity needs to expand as well.

- Promote renewable energy: Second, the transition toward the development of alternative sources of energy needs to accelerate. As long as prices remain high, the incentive to invest in alternative sources of energy will only increase. This is one reason why accusations of price gouging in the energy market ring hollow.

Here’s another way to think of it: If an excessive concentration of power exists inside the energy industry, prices would have increased to these levels long ago. Moreover, prices at these levels will create the conditions for a broader increase in the supply of alternative energy sources, which will bring down demand over the medium to long term.

Price competition is a pre-condition for a functioning market and an increase in choices to supply energy whether the source is oil, natural gas, nuclear, electricity, solar, wind or geothermal. Let that competition begin.

Given geopolitical tensions in Eastern Europe, Asia and the Middle East, a rational energy policy that fosters and develops alternative sources of energy makes every bit of sense.

The takeaway

The U.S. economy, in nominal terms, generates $24.3 trillion annually. Energy is required to sustain the general level of welfare across the economy. We can walk and chew gum at the same time. Increasing the production of fossil fuels and accelerating the transition toward renewables are not mutually exclusive goals. Widening the supply of fuels that support the economy is both necessary and wise.

Let's Talk!

Call us at (509) 455-8173 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-06-09.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/oil-prices-and-price-gouging-deconstructing-the-price-of-gas/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

HMA CPA is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how HMA CPA can assist you, please call (509) 455-8173.